Search

Transport & logistics

BCA is a small regional airport in Belfast, Northern Ireland, located ten minutes by car from Belfast city centre In 2016 it served 2.7m inbound and outbound passengers. Its focus is domestic routes operated by scheduled carriers, serving business as well as leisure customers.

Currently four scheduled carriers (Flybe, British Airways, Aer Lingus and Eastern Airways) serve 17 domestic routes, including London Heathrow and London City. A small part of BCA’s traffic is international: Aer Lingus currently serves four sun routes (although this is due to drop to two) over the summer months; KLM serves Amsterdam; and Icelandair flies to Reykjavik.

Aeronautical revenues (airport charges) are not subject to economic regulation. Commercial revenues are generated principally from car parking, royalties on retail, food and beverage, car hire spend, rental income (lounges and offices) and advertising space.

Over 1,000 people are employed on the site, but only c.70 of those are employed by BCA. Many activities are outsourced (e.g. security, facilities management, air traffic control); and others are provided by third parties on-site (e.g. retail, food and beverage operations and ground handling). Fire services, maintenance, advertising, car parking and administration / management are the main activities that remain in-house.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Communications

DNS:NET is a leading independent telecommunications provider in Germany. Established in 1998, DNS:NET owns the largest independent fibre-to-the-cabinet network in the Berlin area and is rolling out a fibre-to-the home network in Berlin and the surrounding regions.

The company differentiates itself through a superior network, local brand recognition and attractive pricing of high bandwidth products, which drives high customer satisfaction. 3i Infrastructure’s backing will allow DNS:NET to accelerate its build programme to provide gigabit-ready connectivity to its customers.

DNS:NET received investment of £34 million during the year from 3iN to continue the development of its FTTH network in areas around Berlin and in the State of Brandenburg. A new CEO joined DNS:NET in July 2023. He has overseen the preparation of an updated business plan that was agreed with shareholders in December 2023. We are making good progress in building a strengthened and experienced management team.

FTTH network rollouts in Germany remain challenging. Passing homes has been the industry’s primary focus to date. Connecting and activating customers to the network on a timely basis is an industry-wide challenge. The negative value movement in the year was driven by more conservative business plan assumptions for DNS:NET’s FTTH rollout. Throughout the year, DNS:NET has focused on connecting backbone fibre infrastructure and home connections for its owned network, as well as on securing the handover of leased networks built by authorities in the neighbouring State of Saxony-Anhalt, making good progress in the number of its connected and activated customers as a result.

The company is now preparing for the next stages in its network delivery in a way that narrows the time lag between passing homes and connecting and activating customers on that FTTH network to improve performance. We have increased the discount rate to reflect uncertainties over available debt pricing for fibre businesses in future years and the delay against the original rollout timetable.

Energy

ESP is an independent gas transporter (“iGT”) and independent electricity network operator (“iDNO”) providing the ‘last mile’ of connection between properties (predominantly residential, but also industrial and commercial) and the gas and electricity distribution networks.

It focuses on being an ‘independent asset owner’. It acquires (bids for) gas and electricity connections from ‘utility infrastructure providers’ (“UIP”), who have themselves designed and installed the connections for property developers. ESP is then responsible for maintaining the connections going forward and receives a regulated revenue stream for each connection from the gas and electricity companies who charge the end customer as part of their overall gas or electricity bill. Price regulation for both gas and electricity connections is based on the regimes of the gas and electricity distribution companies. Regulation is overseen by Ofgem.

Today ESP owns over 500,000 connections and has an order book for 200,000 more, making it the second largest iGT/iDNO in the UK. ESP also has a domestic metering business (representing almost one quarter of its revenues). Charges for meters are unregulated.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Social Infrastructure

EC Waste is the largest vertically integrated provider of solid waste services in Puerto Rico.

With locations throughout the island, EC Waste provides multiple waste services to over 80,000 residential, commercial, and industrial customers. The company operates four well-located, U.S. EPA permitted disposal sites, which enables EC Waste to serve all of Puerto Rico in an environmentally responsible and sustainable manner. Additionally, the company manages two transfer stations, runs the island’s largest regulated, solid waste collections network and hosts what will be Puerto Rico’s largest renewable natural gas collection project at its El Coqui facility.

3i Group invested in EC Waste in November 2021.

Regulatory information

This transaction involved a recommendation of 3i Corporation.

Energy

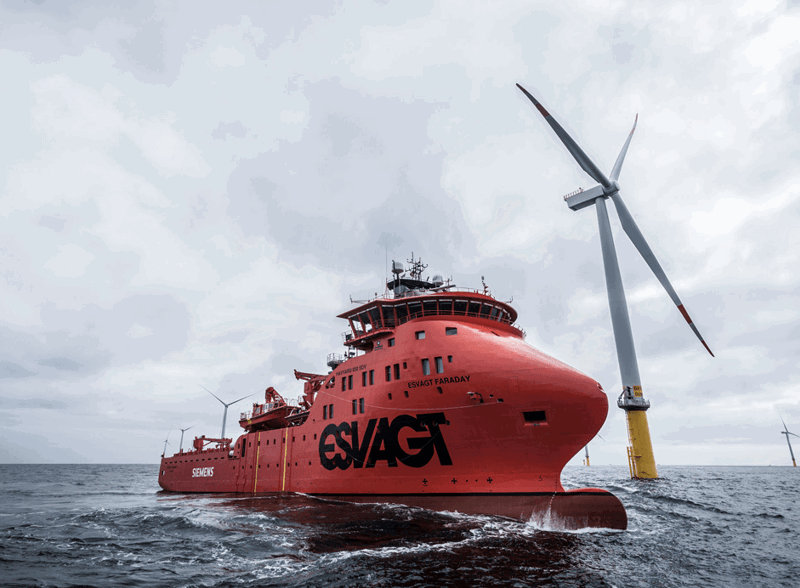

Headquartered in Esbjerg, Denmark, ESVAGT is the market leader in the fast-growing segment of service operation vessels (“SOV”) for the offshore wind industry. The Company is also a leading provider of emergency rescue and response vessels (“ERRV”) and related services to the offshore energy industry in and around the North Sea and the Barents Sea.

ESVAGT is the pioneer and market leader in the provision of SOVs to offshore wind farms, with nine bespoke vessels in operation and a further four under construction. SOVs are purpose-built, high performance vessels, providing efficient transport of maintenance technicians to wind turbines and other offshore wind equipment, under long term contracts. The offshore wind market, and hence demand for SOVs, is expected to grow strongly over the coming years, creating significant opportunities for the company.

Its ERRV services mainly involve the rescue and recovery of personnel, but also include the dispersion and recovery of oil spills, crew transfers and towing. ESVAGT is the leading provider of ERRV services in Denmark and Norway, with market shares of approximately 100% and 50%, respectively, as well as an established and growing presence in the UK. The majority of ESVAGT’s ERRV revenues are associated with North Sea oil and gas production support, with the remainder generated by supporting exploration activity.

ESVAGT has been operating since 1981, employs over 1,100 people and owns a fleet of more than 43 vessels.

ESVAGT performed well in the year, benefitting from strong contract rates and high utilisation levels. As the clear market leader in European offshore wind SOV provision, ESVAGT currently operates nine vessels. A further four SOVs are under construction, specifically designed to serve long-term charter agreements, and construction progress is on track. Despite inflationary pressure causing delays and cancellations in wind farm development, regulators and governments have become more supportive of incentivising growth in offshore wind.

Inflation, while negatively impacting the construction cost of the near-term pipeline, has a positive effect on ESVAGT due to its index-linked contracts, which enhance the value of its operational SOV fleet. The offshore wind market remains on a positive trajectory and this is reflected in the pipeline for additional new SOVs in the North Sea and the rapidly expanding US wind market. Over the next 12 months, we anticipate several tenders to take place.

ESVAGT’s ERRV segment also maintained positive momentum, driven by favourable supply/demand dynamics, and an increased emphasis on security of supply in Europe.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Utilities

Future Biogas is one of the largest anaerobic digestion (AD) plant developers and biogas producers in the UK. It owns two AD plants with one further AD plant in construction, and operates 10 AD plants mainly on behalf of institutional investors under medium-long term contracts.

Future Biogas’s plants convert a wide range of feedstocks into clean and renewable energy through AD which produces biogas. Biogas can either be used to generate green electricity, or upgraded into biomethane and injected into the UK’s national gas network. Future Biogas produces over 500GWh of biogas per year, enough energy for over 40,000 homes.

Biomethane from AD is a ready-to-use and commercially viable solution for hard to decarbonise industrial sectors. It does not require any upgrade to the existing UK gas infrastructure. Energy produced by AD plants is carbon neutral, as the CO2 released during the process matches the CO2 absorbed from the atmosphere by the feedstock.

Future Biogas promotes a regenerative farming approach, sustainably integrating feedstock from energy crops into agricultural systems. The circular process of returning digestate back to land can help replenish soil nutrients and carbon and displaces demand for carbon intensive artificial fertilisers.

Future Biogas performed in line with expectations due to good services revenues and index-linked contracts. The company has a promising pipeline of organic growth and M&A opportunities.

During the year, Future Biogas signed a new 15-year gas supply agreement with AstraZeneca (‘AZ’) for unsubsidised green gas. To deliver this green gas, it is constructing the UK’s first unsubsidised AD plant. In September 2023, 3iN invested £35 million to fund the plant’s construction, which will supply 100GWh of biomethane to AZ’s UK sites.

In November 2023, 3iN invested a further £30 million to fund the acquisition of two AD plants that Future Biogas was already managing. These strategic investments continue to transition Future Biogas from a manager of third-party biogas plants to a leading developer, asset owner and operator. The company is actively exploring viable sites for constructing new AD plants, and the interest from high-quality corporate partners is encouraging.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Communications

Global Cloud Xchange (“GCX”) is a leading global data communications service provider and owner of one of the world’s largest private subsea fibre optic networks. The business provides high-bandwidth connectivity to a range of customers including over-the-top content providers, telecom carriers, new media providers and enterprises.

GCX’s 66,000km of cables span from North America to Asia. It is particularly strong on the Europe-Asia and Intra-Asia routes where it is well positioned to capitalise on growth opportunities and serve the exponentially growing demand for data traffic.

GCX has shown strong year-on-year growth in lease revenues and has recently signed several large bulk capacity deals on its Middle East and intra-Asia subsea routes. Financial performance was held back by a high level of cable cuts which have now been repaired. The sales pipeline is healthy and demand for subsea data capacity continues to grow, driven by increasing adoption of AI applications and substantial investments in capacity and route diversification by the hyperscalers.

Looking ahead, GCX is evaluating several attractive growth opportunities, for example, acquiring new subsea capacity and developing new edge data centres near its cable landing stations that will drive additional data on its subsea network.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Utilities

Herambiente is the Italian leader in the waste treatment and disposal sector. The company owns and operates a portfolio of c.80 waste treatment facilities, mostly located in the Emilia Romagna. The plants include landfills, waste to energy plants, anaerobic digestion and other waste sorting facilities.

Herambiente’s revenues originate primarily from waste treatment and disposal and from sale of the resulting by-products, including electricity from incineration, biogas from landfills and recycled materials. In 2016, Herambiente treated c. 1.7m tons of urban waste, 4.7m tons of special waste and produced 161,455,167kWh of electricity.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Utilities

Infinis is the UK’s leading generator of low carbon power from captured methane. The business captures methane gas from landfill sites and disused mines and converts it into electricity. Its sustainable energy expertise also includes solar power and battery energy storage technology. This work helps to reduce the impact of greenhouse gas emissions on climate change and provides secure, efficient local power generation.

Infinis’s cashflows are positively correlated with UK inflation through the Government-backed Renewables Obligations Certificate (ROC) and CfD regimes and through index-linked corporate PPAs. Infinis’ current generation portfolio comprises:

This unique combination of green baseload power, renewable assets and flexible generation mean Infinis is ideally placed to respond to growing electricity demand, increasing energy market volatility and to play a key role in the UK’s route to decarbonisation and greenhouse gas reduction.

Infinis had a strong financial performance despite lower UK power prices. It generated a value gain of £20 million as its captured landfill methane business outperformed expectations, compensating for lower margins from its power response assets. Furthermore, Infinis is making significant progress in developing its 1.4GW solar energy generation and battery storage pipeline, with 103MW of solar capacity already operational.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Social Infrastructure

Ionisos is a leading owner and operator of cold sterilisation facilities servicing the medical and pharmaceutical industries. Established in 1993 in France, Ionisos is one of the largest cold sterilisation providers globally and operates a network of 11 facilities in Europe with market leading positions in France and Spain. It has over 250 employees and a highly diversified customer base of around 1,000 customers.

Ionisos delivers a mission-critical, non-discretionary service for customers, for whom cold sterilisation is an essential component of the manufacturing process. It is typically applied to single use products that would be damaged by the heat and/or humidity of hot sterilisation methods.

Ionisos performed below expectations due to reduced bio-processing and labware volumes, which have returned to pre-Covid levels, and weaker demand in markets connected to the construction industry which represents a small share of treatment capacity. However, the majority of product categories sterilised by Ionisos continue to exhibit strong volume growth. Ionisos is making progress in its growth initiatives. The expansion of its new greenfield EO plant in Kleve, Germany is progressing and the development of the new X-ray greenfield facility in north east France is proceeding according to schedule and within budget.

Energy

Joulz is a leading owner and provider of essential energy infrastructure equipment and services in the Netherlands. Joulz serves approximately 21,000 industrial, commercial, and public sector clients with its solutions, that encompass realization, maintenance, management, and leasing of energy infrastructure equipment.

Joulz’ service offering includes mid-voltage infrastructure (owning and leasing transformers, switchgear and cables under long-term contracts), storage (owning and leasing large scale battery storage systems under mid- to long-term contracts), solar (large-scale installations under operational lease or with government-subsidized PPAs), metering (owning and leasing 50,000 electricity and gas meters under mid-term contracts) and EV charging (AC and DC charge points in mid-term exploitation, rental or CPO contracts). Additionally, it provides integrated solutions to address energy transition challenges such as grid congestion.

Joulz performed in line with expectations. It is benefitting from its inflation-linked longterm contracts and the completion of new installations. Joulz has seen significant interest in integrated energy transition solutions from customers seeking to decarbonise their operations and overcome constraints due to electricity grid congestion.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Transport & logistics

Oystercatcher is the holding company through which 3i Infrastructure holds a 45% interest in Advario Singapore Limited (previously Oiltanking Singapore Limited).

Advario Singapore is a 1.3 million cubic metre facility focused on storage and blending of refined clear petroleum products for a range of blue chip customers. With a premier location, on Jurong Island, it is accessed by pipeline, sea going vessel and barge.

Oiltanking is one of the world’s leading independent storage partners for oils, chemicals and gases, operating 41 terminals in 18 countries with a total storage capacity of 16 million cubic metres.

Oystercatcher performed well in the year. Advario Singapore, which is 45% owned by Oystercatcher, benefitted from high utilisation levels for its storage capacity, high customer activity levels and higher rates being secured at contract renewal. Whilst the oil products market remains in backwardation, a tight storage market in Singapore and the wider region provided a helpful backdrop to renewal discussions. Advario Singapore remains the leading gasoline blending facility in Singapore and the wider region.

The company has continued to pursue opportunities linked to sustainable fuels, in line with its sustainability strategy. Building on its success to date with Neste, which is blending sustainable aviation fuel (‘SAF’) at Advario Singapore, the terminal had actively looked to expand its role in activities to supply sustainable transport fuels.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.

Transport & logistics

Formed in 2007, Regional Rail provides freight transportation, car storage, and transloading services in New York, Pennsylvania, and Delaware across three railroads and over 155 miles of track connecting to a diversified Class 1 railroad network.

In 2018, the company moved over 13,000 carloads while serving over 70 customers across a diversified set of end-user markets including heating, fuel blending, agriculture, chemicals, and metals. The company’s wholly owned subsidiary, Diamondback Signal, is the premier provider of rail-crossing installation and maintenance services to over 100 short-line rail customers across 20 states.

In October 2019, Regional Rail acquired Pinsly Railroad Company’s Florida operations adding 208 miles of track across three short-line railroads.

Regulatory information

This transaction involved a recommendation of 3i Corporation.

Transport & logistics

Headquartered in White Bear Lake, Minnesota, Smarte Carte is the leading provider of self-serve vended luggage carts, electronic lockers, commercial strollers and massage chairs at more than 2,600 locations worldwide. For luggage carts, SmarteCarte is the sole provider in 125 locations, including 49 of the top 50 airports in the U.S. The company's products can be found in amusement parks, fitness clubs, shopping malls and ski resorts.

Regulatory information

This transaction involved a recommendation of 3i Corporation.

Transport & logistics

SRL is the market leading temporary traffic equipment (“TTE”) rental company in the UK. SRL offers its customers a full-service rental solution, which includes the planning and design of traffic management systems, installation, maintenance and integration with existing systems, as well as direct sales of equipment assembled by SRL.

SRL’s market-leading reputation is supported by its national depot network, providing a 24/7, 365 days a year service on which customers rely for quick deployment and reactive maintenance work.

SRL performed slightly behind expectations during the financial year. There has been a reduction in general market activity levels due to delays in capital expenditure programmes within the public sector in advance of the UK general election, and in the telecom sector as the fibre rollout has slowed.

Despite this challenging market environment, SRL has shown resilience and continued to grow its revenue and EBITDA. It has also been successful in extending contract durations with customers, providing better revenue visibility.

Communications

Tampnet is the leading independent offshore communications network operator in the North Sea and the Gulf of Mexico. It is headquartered in Norway, with operations in the UK, Scandinavia and the USA.

Tampnet provides high speed, low latency and resilient data connectivity offshore through an established and comprehensive network of fibre optic cables, 4G base stations, and microwave links. It operates across four main business areas: fixed installations, mobile rigs and vessels, roaming for offshore workers and international carriers. The majority of its business involves providing fixed fibre links to oil platforms.

Tampnet performed extremely well in the year, generating a value gain of £54 million. It exceeded revenue and EBITDA targets, driven by increased offshore activity and stronger demand for bandwidth upgrades.

Tampnet is continuing to expand its network infrastructure by pursuing new fibre projects in both the North Sea and the Gulf of Mexico. Notably, Tampnet secured significant new contracts in these regions.

Digitalisation of the offshore energy sector is gaining momentum and Tampnet’s digitisation proposition, which combines low-latency connectivity with services such as private networks, is generating considerable interest.

Tampnet’s private networks offer a secure, closed 4G/5G system deployed on offshore platforms, providing robust connectivity and enhanced security compared to traditional Wi-Fi solutions.

Furthermore, Tampnet is actively engaged in carbon capture and offshore wind projects within its existing network in the North Sea. The business was awarded its first offshore carbon sequestration connection in March 2024. The potential for further comparable initiatives is substantial and Tampnet is strategically positioned to contribute to their success.

Regulatory information

This transaction involved a recommendation of 3i Investments plc.